Weekly Update June Monday 21st 2021

Four in ten retirees fail to claim pension credit

Low-income pensioners are continuing to miss out on thousands of pounds of benefits as they fail to claim pension credit.

According to official figures, £1.6bn in pension credit is going unclaimed each year with nearly 1m pensioner households missing out on an average £1,600.

Pension credit take-up is the lowest of all means-tested benefits, with 40 per cent of those eligible failing to claim.

Take-up of pension credit has been around 60 per cent since 2010 and government efforts to improve it have not helped.

Pension credit tops up single pensioners’ income to £177.10 a week and £270.30 for couples.

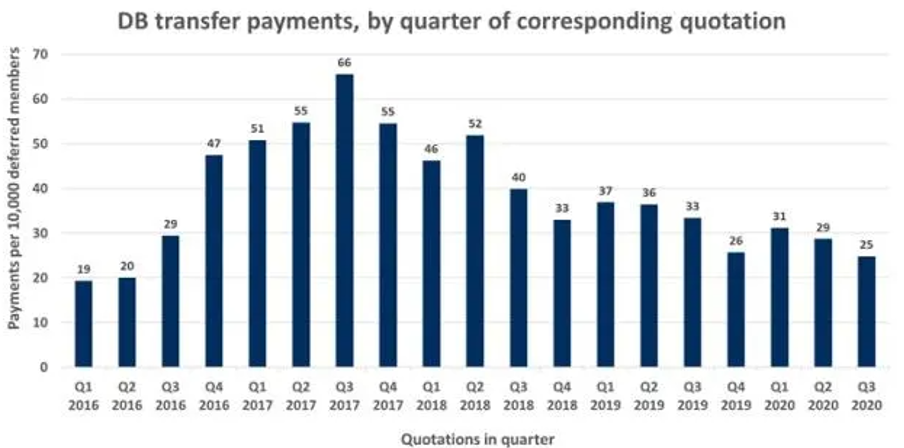

DB transfers fall to lowest level in 5 years

Defined benefit transfers have fallen to their lowest level in five years, with only one in 400 members transferring out, as the contingent charging ban appears to have taken a toll.

Analysis from LCP, published today (June 14), found in Q3 2020 only 25 out of every 10,000 members transferred out of their DB pension into a defined contribution plan, down 62 per cent from the peak in Q3 2017 and the lowest level since 2016.

Data from Q3 is the latest available due to the lag between a quotation being issued and the corresponding payment being made, which can be between three and six months, LCP said.

The consultancy said although transfer activity has been on a gradual decline, the latest falls could be directly linked to the ban on contingent charging which came into force in October 2020.

The ban on contingent charging means a client has to pay for the advice regardless of whether they go on to transfer.

It applies to all transfers apart from consumers with certain identifiable circumstances, such as those suffering from serious ill-health or experiencing serious financial hardship.

How can we stop savers from doing nothing at all?

Last month the Financial Conduct Authority released a consultation titled “The stronger nudge to pensions guidance”, proposing to make it mandatory for providers to offer consumers a final opportunity to take Pension Wise guidance at the point they wish to access their pensions savings. With only around 10 per cent of the UK adult population currently taking financial advice in any form, is guidance rather than professional advice going to produce the desired outcome of financial security and wellbeing in retirement? On its own, probably not. However, the vast majority of savers remain unsupported or reliant on guidance services that, while welcome and useful, cannot adequately prepare an individual to make financial decisions that could have ramifications for more than 30 years.